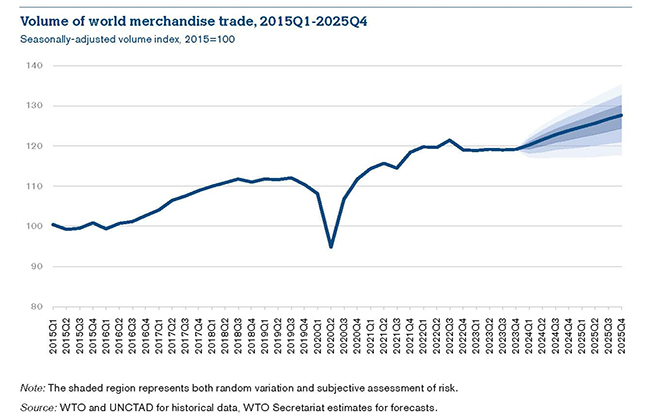

The latest edition of the WTO’s “Global Trade Outlook and Statistics” foresees a gradual recovery in world merchandise trade volume in 2024 and 2025. This follows a contraction in 2023 driven by the lingering effects of high energy prices and inflation in advanced economies, particularly Europe. So, what does our forecast indicate?

Specifically, we expect merchandise trade to grow by 2.6% in 2024 and 3.3% in 2025 after falling by 1.2% in 2023. However, there is a downside risk due to regional conflicts, geopolitical tensions and economic policy uncertainty.

In value terms, merchandise trade fell 5% in 2023 to US$ 24.01 trillion but the decline was mostly offset by a 9% increase in commercial services trade, which reached around US$ 7.54 trillion. Total goods and services trade was only down 2%.

A particularly bright spot for services was the global exports of digitally delivered services, which reached US$ 4.25 trillion in 2023, up 9% year-on-year, accounting for 13.8% of world exports of goods and services.

The value of these services — meaning services delivered digitally across borders through computer networks, and encompassing everything from professional services to streaming of music and videos, and including remote education — surpassed pre-pandemic levels by over 50% in 2023.

In terms of merchandise trade volume, most of the decline between 2022 and 2023 was driven by Europe, which subtracted 1.7 percentage points from global import growth and reduced global export growth by 1.0 percentage points.

However, looking ahead, we expect all regions to make positive contributions to export and import growth in 2024. In particular, Asia is expected to add around 1.3 percentage points to global export growth and 1.9 percentage points to global import growth in 2024.

However, regional conflicts and geopolitical tensions could limit the extent of the trade rebound by causing further price spikes in food and energy prices.

For example, although the Suez Canal disruptions stemming from the Middle East conflict have been relatively limited so far, some sectors, such as automotive products, fertilizers and retail, have already been affected by delays and freight costs hikes.

It also appears that geopolitical tensions are beginning to affect trade patterns, with 30% less growth in bilateral trade between the United States and China than in their trade with the rest of the world since 2018.

Moreover, trade between hypothetical blocs of geopolitically aligned countries has been growing 4% more slowly than trade within blocs since the beginning of the war in Ukraine.

However, while the trade environment is clearly challenging, we should not paint too dark a picture of international trade. The volume of world merchandise trade was essentially flat throughout 2023, and the 1.2% decline in 2023 is relative to 2022. In fact, it was up 6.3% compared to the pre-pandemic peak in the third quarter of 2019, and up 19.1% compared to 2015. These figures emphasize the resilience of international trade.

Trade growth in 2023 was unusually weak compared to real GDP growth at market exchange rates, which only slowed to 2.7% in 2023 from 3.1% in 2022. It is expected to remain stable over the next two years at 2.6% in 2024 and 2.7% in 2025.

We believe that inflation was an important driver of this. Higher prices depressed real household incomes and eroded net revenues of firms in 2023, reducing demand for manufactured goods, which feature disproportionately in international trade. Europe was hit especially hard by the rising cost of energy since the start of the war in Ukraine, due to its dependence on imported natural gas.

However, inflationary pressures are expected to abate this year, allowing real incomes — particularly in advanced economies — to grow again. This should boost the consumption of manufactured goods. A recovery in the demand for tradable goods in 2024 is already evident from new export orders, which point to improving conditions for trade.

Easing inflationary pressures and eventual reductions in interest rates should gradually lift consumption and raise import demand in 2024 and 2025.